3 Dividend Growth Stocks I Bought In February

3 Dividend Growth Stocks I Bought In February

There has been positive reception to these blog posts that I’ve been doing. For interested readers, you can subscribe and every time a post is published you will get an email with the article! There is a paid subscription option (thanks for the additional support for those choosing this option allows me to continue to dedicate my time here!), but there is no benefit at this time. Just choosing the free option will still allow the same access.

Every month I make some purchases. On Seeking Alpha I mostly focus on closed-end funds, and everything related to those investment vehicles there. Through there I publish a monthly article on what I’m buying in the CEF space. Now that I have this other outlet for writing, I thought that there might be some interest to share what I’m buying in the individual stock space!

I make purchases every month because I’m a long-term investor. I’m already at my upper cash limit of around 12% where I feel comfortable. There is a huge opportunity cost of sitting in too much cash for too long. Markets can remain elevated and irrational for extended periods of time. Thus, a lot of months and quarters can go by when I could be collecting dividends and reinvesting. Which then only compounds and translates into even more dividends and cash flow coming in.

In fact, this strategy works even better when markets are in a panic mode such as last March’s COVID-induced rattling of the market. This is because you can buy even more shares due to lower prices. Of course, we were incredibly fortunate at the swift rebound. Had the market still been struggling after a year, I believe we would have seen more dividend cuts overall. That would have translated into lower-income year-over-year as opposed to a healthy increase in my income derived from dividends YoY!

With that out of the way - these are the three dividend stocks I bought and a bit of information on them!

(Source)

AbbVie (ABBV)

I don’t think this one is a surprise. I had been assigned those puts we wrote at the end of January and come Monday morning on February 1st, I was put the shares. Of course, this was an okay outcome and one we knew could happen. We’ve since been writing covered calls against this sleeve of the shares. I have held ABBV shares even before being assigned these shares.

Before writing those puts, we knew that ABBV was gearing up to release its earnings for Q4 and full-year results. They did so on February 3rd and beat on both EPS and revenue estimates.

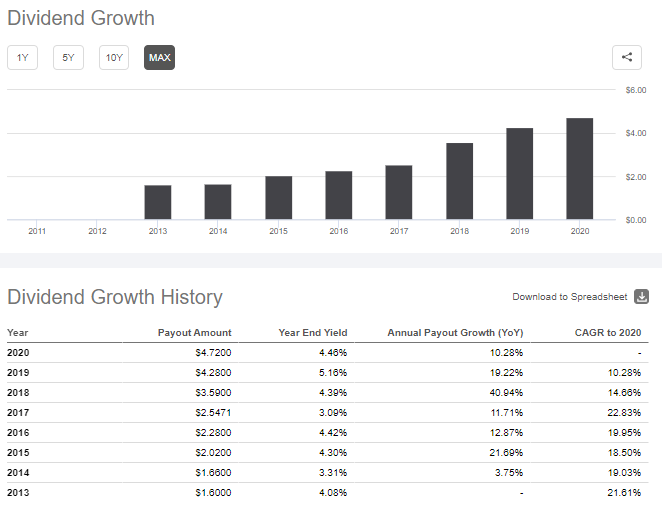

They also announced their next dividend on February 18th, it is payable on May 14th, 2021. They boast that the dividend has increased by 225% since ABBV was spun off in 2013. The dividend works out to 4.82% currently.

(Source - Seeking Alpha)

ABBV continues to make strides against its dependence on Humira. Which still accounts for the largest share of their revenue.

Realty Income Corp (O)

This company needs little introduction for dividend investors or REIT investors. While most retail is dead at this point (malls especially.) O offers a bit of a reprieve from the dreary-looking retail picture.

This is because they focus on mostly better assets. A lot of their top clients did not have to shut down during the pandemic as they are considered essential services. They have only benefited from shutdowns over the last year, in fact. As consumers were essentially forced to these large chains.

That isn’t to say every top client of O’s portfolio was in the same boat. Regal Cinemas and AMC Theaters both account for 2.7% of their mix or 5.4% together. They certainly were not at the end of benefiting from lockdowns.

(Source - Company Website)

Every dividend investor knows of O and the appealing monthly dividend. They raise this dividend quarterly too. This appeal over the years has driven the dividend yield down to about 4.63%. Up a considerable amount from ~2019 when the stock was trading much higher, but still relatively low for a REIT that has to contend with Treasury yields. Sharper moves higher in Treasuries can continue to put short-term pressure on this name. Despite this, I’m content on holding and continuing to accumulate at various times over the longer-term.

STAG Industrial Inc (STAG)

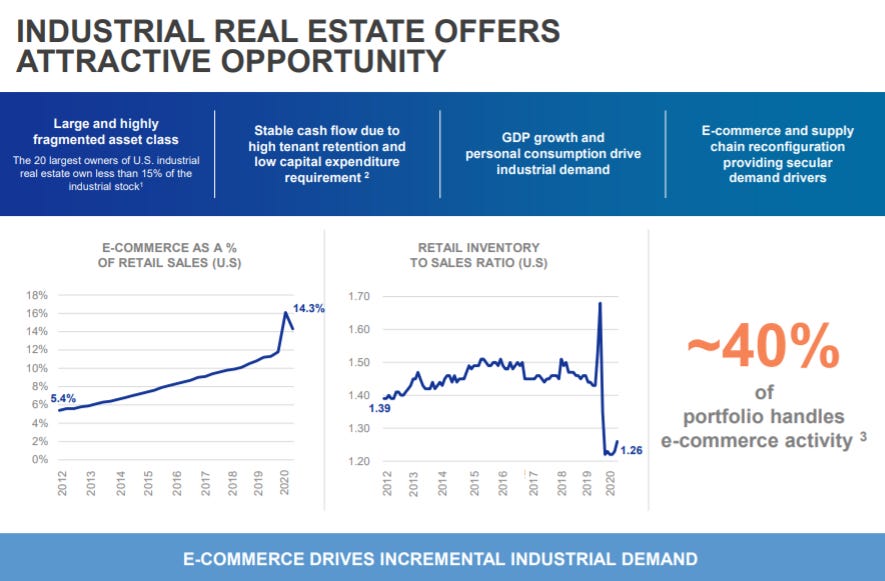

STAG Industrial, Inc. (NYSE: STAG) is a real estate investment trust focused on the acquisition and operation of single-tenant, industrial properties throughout the United States. By targeting this type of property, STAG has developed an investment strategy that helps investors find a powerful balance of income plus growth.

STAG is another monthly paying dividend REIT. This time, they aren’t investing in ‘dead’ retail that should be avoided at all costs. They are investing in warehouses and facilities to facilitate the expanding needs to storing and shipping online goods. That is about the opposite of investing in retail. The shift from shopping at physical locations to online has only increased in the last year due to lockdowns. They offer diversified exposure across the whole U.S. Meaning that they aren’t tied to any particular regional risk.

(Source - Company Presentation)

Though their dividend growth is rather lacking. It isn’t non-existent, but definitely lacking. Going back to about 2013 they increase their dividend annually but from 2015 and beyond it has been at $0.001 - a tenth of a cent raise. The current dividend yield still works out to an appealing 4.53% - though they too have to compete with Treasury yields rising.

The difference here that STAG is growing faster than O at the moment, and should continue to do so. I suppose if you ran a $22.62 billion market cap REIT as O does, you’d have trouble growing as well. In contrast, STAG’s market cap is $5.12 billion. So they can be a bit more agile.

Disclosure: Long ABBV, O, STAG

This is not investment advice but for entertainment purposes only. Any decision to buy or sell is solely made by that individual. Speak with a financial professional to develop an investing plan that is right for your own objectives and goals.