Collecting More AbbVie Premium, Ex-Date Coming Up For This ~5% Yielder

Collecting More AbbVie Premium, Ex-Date Coming Up For This ~5% Yielder

Thank you for reading this article. Consider subscribing to get notified of future posts. There is a paid option, though for now, I’m posting everything free.

(Source)

AbbVie (ABBV) is a popular dividend growth stock. It is a biopharma company that gets a lot of attention. The main attention comes from the fact that Humira remains a key component of the companies total revenue. They have been working on this through various efforts and making progress.

The company was a spinoff from Abbott Laboratories (ABT). Since then they have been growing their dividend without missing a beat. An attractive characteristic considering that ABT itself has a long history of growing its own dividend too. They have grown their dividend for 49 years and are a member of the S&P 500 Dividend Aristocrats Index.

Today I’m looking at primarily how I’ve been able to collect even more “income” from ABBV through writing puts and covered calls.

Writing Call, Collecting Premium - And Dividend Talk

We once again are selling calls on our ABBV position. Previously, the shares fell quite rapidly but have been clawing their way back higher. To me, the stock is still at an incredible value at a forward P/E of just 8.53. Of course, it is being punished on Humira concerns going forward. That latest FDA announcement extending the review of their Rinvoq drug is what dropped the price previously.

(Source - Google Finance)

As a biopharma company, ABBV is prone to these wild swings based on FDA announcements; approvals, rejections or extensions of reviews. This can make the company a bit more uncertain for income investors. Though the large and rapidly growing dividend is one of the draws for ABBV in the first place. They’ve been growing it since their spinoff from ABT. As we get closer to 2023, I suspect that we will continue to see volatility.

(Source - Seeking Alpha)

The next ex-date is coming up quite soon for ABBV as well. If you own the stock before 4/14/2021, you will be entitled to the next $1.30 dividend payment. If all goes well, with our latest trade it won’t necessarily matter if we collect the dividend or not. Though the expiration we used this time was April 9th, 2021. A mere 11 days away and lower on the annualized return of only around 8% if we were doing this naked.

I wrote the trade at a strike of $111 collecting $0.27 or $27 per contract. If you remember way back in January, we were put the shares at $110. Thus, we have the shares and it isn’t a naked trade. Meaning that the annualized figure above isn’t necessarily the most accurate in our case. Though it is a standard way of measuring return. (Premium collected divided by the strike and annualized if we could do this same trade every single 11 days.) In my mind, that would be collecting the dividend just via appreciation if it happens.

Of course, I would be more than happy to collect this premium and the dividend as well. This $0.27 per share is now added to our total $2.61 in premiums that we have collected along the way. This is added up and brings us up to $2.88 per share in premium collected.

In terms of the dividend payout, that works out to 41.85%. To me, that isn’t a stretch in paying the dividend at all.

Dependence On Humira Is Being Worked On

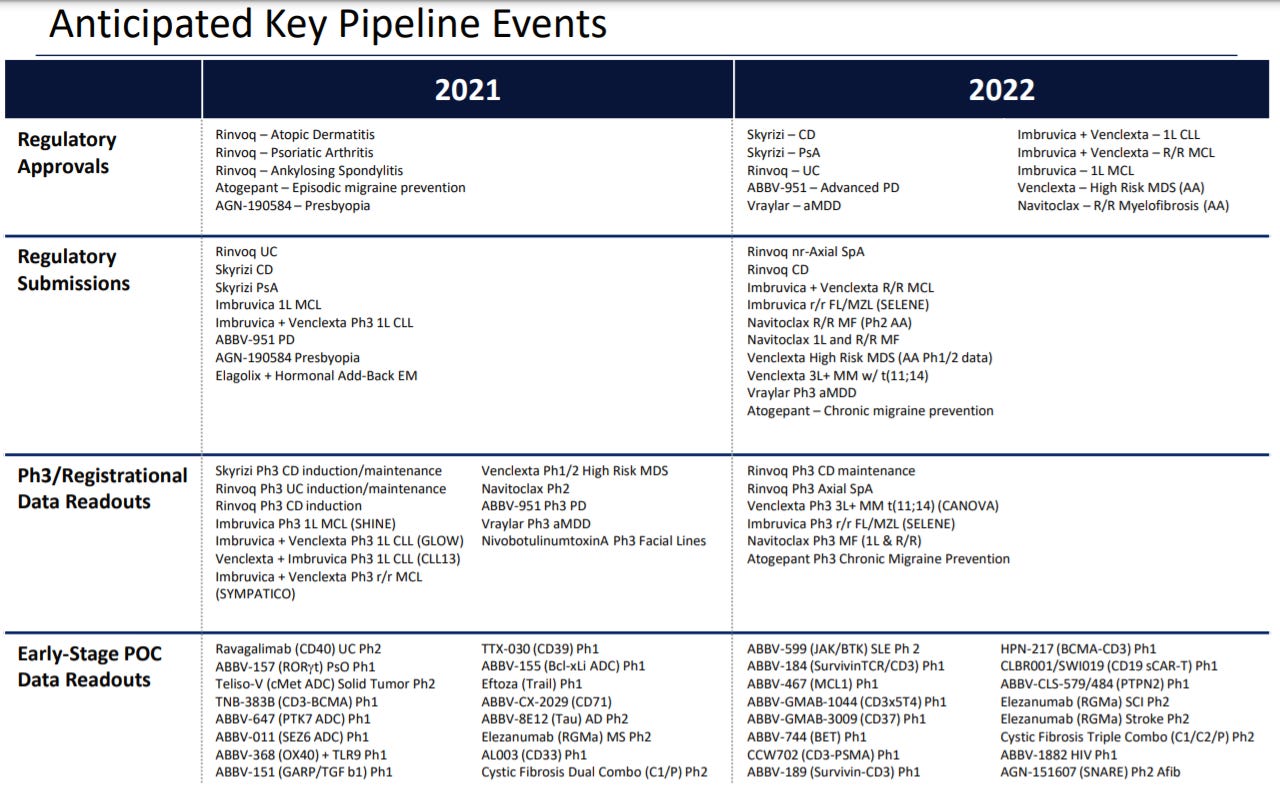

While Humira continues to be a top earner for the company; several other candidates are growing considerably. Skyrizi and Rinvoq both grew sales by over 100%. Venclexta also is growing considerably, and a larger seller, Imbruvica, is growing too. They recently gave an update on “Anticipated Key Pipeline Events” that we can look forward to over 2021 and 2022.

(Source - ABBV Presentation)

This is also why ABBV acquired Allergan last year to help get away from the dependence on Humira and transform the company. Repositioning for the future.

For the full-year ending December 31st, 2020 - Humira’s net revenues accounted for ~43.3%. In the U.S. it was still a driver of growth. Though we see that internationally it was a decline of 7.9% in revenue. Of course, due to the patent and biosimilar pressures. A year earlier, Humira was 57.6%+ of 2019’s adjusted net revenues.

ABBV 2021 Outlook

The outlook for ABBV remains strong. They are weaning themselves off the Humira drug… They anticipate that EPS for the full-year 2021 will be in the $6.69 to %6.89 range on a GAAP basis. For the adjusted diluted EPS they anticipate the full-year being between $12.32 to $12.52. In this case, “2021 adjusted diluted EPS guidance excludes $5.63 per share of intangible asset amortization expense, non-cash charges for contingent consideration adjustments and other specified items.”

Intangible just simply means something that isn’t physical - like goodwill or in the case of biopharma companies, looking at patents. Physical assets depreciate, and intangible assets amortize.

For 2020, they had adjusted diluted EPS of $10.56. That means they are expecting EPS to grow ~17.6% for the year. This should bode well for supporting further dividend growth, a key feature that income investors are probably noting.

Conclusion

ABBV might be on the riskier side for most income investors. Primarily due to the volatility that biotech stocks experience; though ABBV’s pharma business can help dampen the effects too. That being said, it has produced some solid results and has been able to grow its dividend. Over the next couple of years, we will really see if management is earning their pay if they can navigate this company successfully. For now, I’m happy to be long the shares and trade around this one with options, enhancing the “income” generation through collecting premiums.

Disclosure: Long ABBV

This is not investment advice but for entertainment purposes only. Any decision to buy or sell is solely made by that individual. Speak with a financial professional to develop an investing plan that is right for your own objectives and goals.